Building wealth sounds great, right? But why does it feel so hard? It turns out that many of us unknowingly make common money mistakes that prevent us from reaching our financial goals. These small but significant errors add up, making wealth seem farther away than it should be.

This article breaks down seven major money mistakes that are holding you back and, more importantly, how to avoid them. Let’s dive in!

Introduction: What’s Keeping You from Building Wealth?

Most of us dream of becoming financially independent—whether that means living comfortably without stressing about bills, being able to travel, or just retiring early. But have you ever wondered why it seems so hard to get ahead financially?

Often, it’s because of small mistakes we make without even realizing it. These mistakes keep adding up over time, stopping us from saving, investing, and growing our wealth. So, let’s look at the seven biggest money mistakes and how to avoid them!

Mistake 1: Living Paycheck to Paycheck

Why People Fall Into This Trap

Living paycheck to paycheck means your money is gone by the time your next paycheck arrives. It’s a stressful way to live and makes it impossible to save for the future. So why does this happen? For many, it’s because they’re spending without a plan or relying too much on credit.

Breaking the Cycle

The first step to getting out of this cycle is knowing exactly where your money is going. Track your expenses for a month and look for areas where you can cut back—whether it’s dining out, streaming subscriptions, or impulse purchases. Once you’ve freed up some cash, start saving and building a financial cushion.

Mistake 2: No Real Budget

Why Budgeting is Key

If you don’t have a budget, you don’t have a clear view of where your money is going. A budget isn’t meant to restrict you—it’s actually the opposite! It gives you control over your money and ensures you’re spending on things that matter.

Simple Steps to Create a Budget

An easy way to start is by using the 50/30/20 rule:

- 50% of your income goes to essentials (rent, utilities, food)

- 30% goes to discretionary spending (entertainment, shopping)

- 20% goes to savings and paying off debt

This method is flexible and helps you balance your financial priorities.

Mistake 3: Skipping an Emergency Fund

Why You Need One

Life is unpredictable—emergencies happen! Car repairs, medical bills, or losing your job can all put you in a tough spot financially. An emergency fund is there to save you from having to borrow money or dip into your savings for these unexpected expenses.

How Much to Save

Experts suggest setting aside three to six months’ worth of living expenses in an emergency fund. If that sounds intimidating, start small! The important thing is to begin putting something away, even if it’s just a little bit at a time.

Mistake 4: Ignoring Debt

The Snowball Effect of Debt

Debt, especially high-interest credit card debt, can snowball quickly. You miss a payment or make the minimum payment, and suddenly your debt grows even faster. Ignoring it won’t make it go away, but there are smart strategies to handle it.

Smart Ways to Tackle Debt

There are two main ways to pay off debt:

- The Snowball Method: Start by paying off your smallest debts first to build momentum, then tackle the larger ones.

- The Avalanche Method: Focus on paying down debts with the highest interest rates first to save the most money over time.

Both methods work, so pick the one that keeps you motivated!

Mistake 5: Overspending on Your Lifestyle

Lifestyle Creep: What It Is and How It Hurts

Lifestyle creep happens when your spending goes up as your income goes up. You get a raise, so you start buying more expensive things—upgrading your car, eating out more often, or buying designer clothes. Over time, this can drain your finances, leaving you with less money to save or invest.

Practicing Mindful Spending

To prevent lifestyle creep, be mindful of your purchases. Ask yourself if you really need something or if you’re just spending because you can. Try to keep your lifestyle the same even as your income increases, and funnel that extra money into savings or investments instead.

Mistake 6: Not Investing Early

Why Time Is Your Best Friend in Investing

The earlier you start investing, the more time your money has to grow. This is due to compound interest, where you earn interest on both your initial investment and the interest you’ve already earned. Over time, this can lead to exponential growth in your wealth.

Easy Ways to Start Investing

If you’re new to investing, start with low-risk options like index funds or mutual funds, which spread your money across many different stocks. These are less risky than investing in individual stocks and are great for beginners. And don’t wait—start now!

Mistake 7: Not Planning for Retirement

The Importance of Early Retirement Planning

Many people put off planning for retirement because it seems far away. But the truth is, the earlier you start, the easier it will be to retire comfortably. Without a solid retirement plan, you might find yourself struggling in your later years.

Steps to Get Started

- Figure out how much you’ll need to live comfortably in retirement.

- Start contributing to a retirement account like a 401(k) or IRA as soon as possible.

- Take advantage of employer matching programs if available—this is free money!

Avoiding These Mistakes Moving Forward

The key to avoiding these common money mistakes is awareness. Now that you know what to look out for, you can make smarter financial decisions. Review your current habits and make small adjustments. Set up automatic savings, stick to a budget, and make sure you’re investing for the future.

Building a Healthy Financial Mindset

Your mindset plays a huge role in your financial success. Building wealth isn’t just about earning more money—it’s about how you manage it. Cultivating a wealth mindset means thinking long-term, focusing on growth, and viewing financial setbacks as learning opportunities.

Money Myths That Hold You Back

There are a lot of money myths that can hold you back. For example, many people believe they need a huge salary to start investing, or that they’ll always be in debt. These false beliefs can limit your financial potential. Bust these myths and adopt healthy financial habits instead!

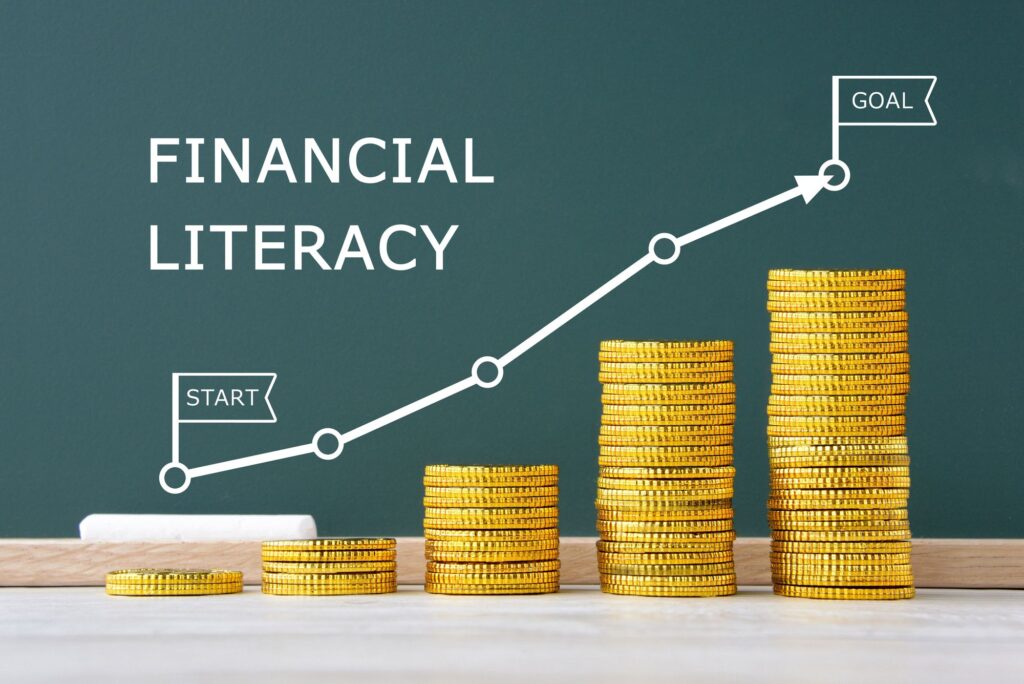

Why Financial Education Is Key

Understanding how money works is crucial to building wealth. Many people make costly mistakes simply because they don’t know any better. Take the time to educate yourself on topics like budgeting, investing, and managing debt, and you’ll be much better equipped to achieve financial success.

How Small Financial Habits Make Big Changes

The little things add up. Cutting out small expenses, like daily coffee or takeout meals, can lead to significant savings over time. Even small changes in your spending, saving, and investing habits can have a big impact on your financial future.

Conclusion: Take Control of Your Finances

Achieving wealth isn’t about luck or earning a massive salary—it’s about being intentional with your money. By avoiding these seven deadly mistakes, you can set yourself on the path to financial freedom. Start making small changes today, and you’ll be surprised at how far they can take you.

Do follow our Instagram page https://shorturl.at/r3sO3 to learn more about money stuffs!

5 Common FAQs

- What’s the easiest way to stop living paycheck to paycheck?

Track your spending, cut unnecessary expenses, and prioritize saving. Creating a budget is the first step toward breaking the paycheck-to-paycheck cycle. - How can I start investing with little money?

Start with low-cost options like index funds or mutual funds, and begin investing whatever amount you can afford. The important thing is to get started! - How much should I have in my emergency fund?

Experts recommend saving three to six months’ worth of living expenses. - What’s the best way to pay off debt?

The snowball method (paying off small debts first) and the avalanche method (paying off high-interest debt first) are both effective strategies. - When should I start planning for retirement?

Start as early as possible, even if retirement seems far away. The sooner you begin, the more time your investments will have to grow.

YOU May Also Like: